Disclosures come home to roost

Disclosures come home to roost

At long last, the Capital Markets can report

ESG has been around for nearly 20 years, but it wasn’t until a few years ago that it gained widespread attention. It was as if a klaxon sounded on the devices of all CEOs globally. Larry Fink, CEO of BlackRock’s annual CEO letter in 2018, titled “A Sense of Purpose,” wrote:

I want to reiterate our request, outlined in past letters, that you publicly articulate your company’s strategic framework for long-term value creation and explicitly affirm that it has been reviewed by your board of directors.

The letter made waves with the corporate elite at Davos that year and marked a shift in attention towards sustainability and social topics in business. From here, we had the start of voluntary disclosure consolidation and the stellar corporate growth of ESG data. And, of course, more annual CEO letters.

Most companies accelerated their reporting efforts, with an intense focus on emissions since climate change is so pressing, and the guidance for the GHG Protocol has been in place for years. Much of a company’s emissions sit in Scope 3, or the emissions from their value chain. Some industries have extremely complex Scope 3 emissions. For example, an auto manufacturer has to consider the carbon upstream from parts suppliers, the logistics of delivery of components to the factory, and then the downstream use of the sold products.

In other words, every industry has different material intersections with emissions.

Yet, there is one industry that is incredibly difficult to measure due to the sheer scope and dependence on others’ reporting. It’s the one that started this focus: financial services, but more specifically, capital markets. The industry that begged for comparable data to move capital around is finally getting a standardized way to report.

PCAF organizes reporting for the markets

One of the ways anything related to ESG gets done is through consortiums. For financial services, the Partnership for Carbon Accounting Financials, or PCAF, “is a global partnership of financial institutions that work together to develop and implement a harmonized approach to assess and disclose the greenhouse gas (GHG) emissions associated with their loans and investments.”

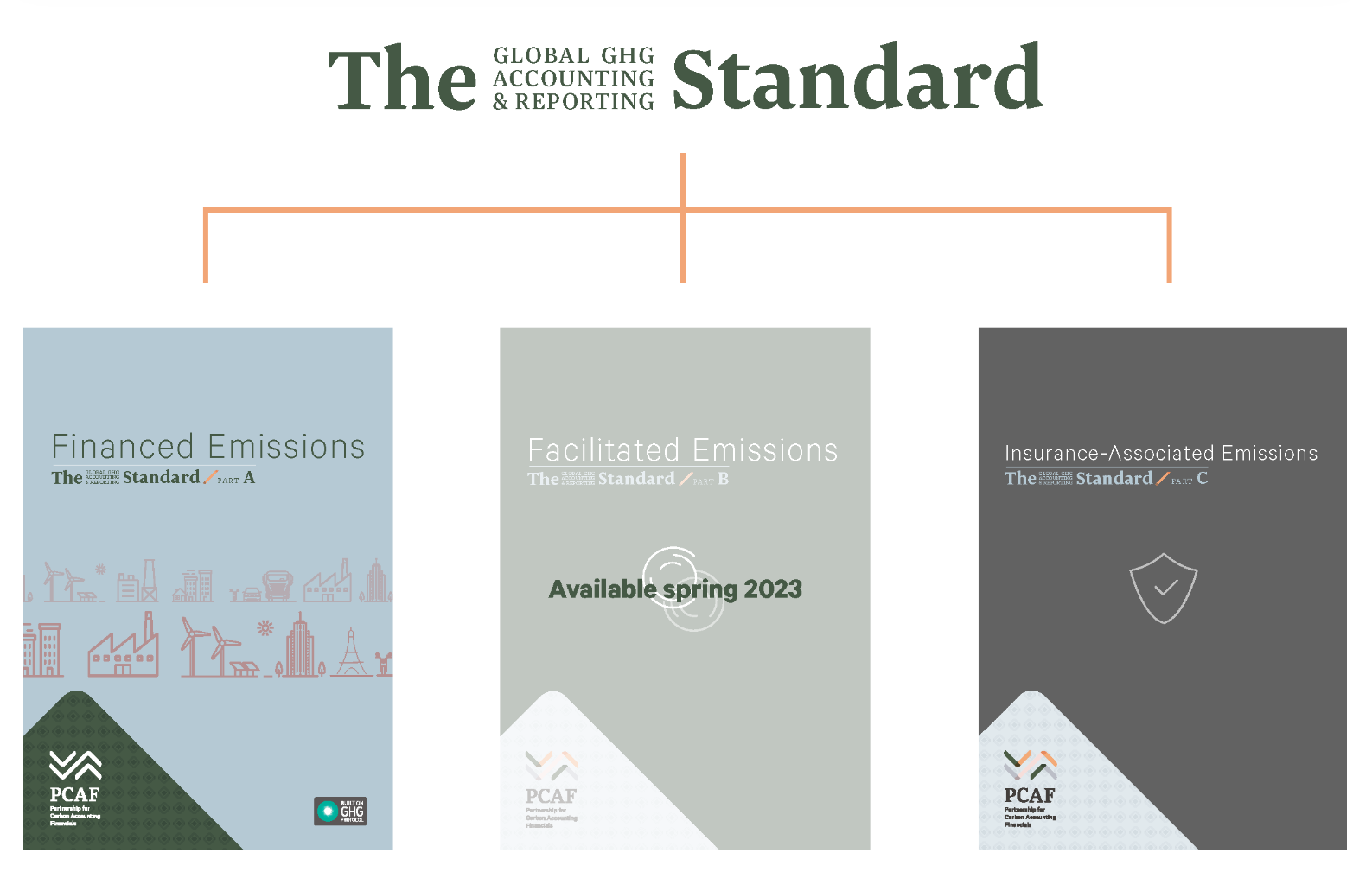

In recent years, PCAF has created two standards associated with Scope 3, Category 15.

PCAF Part A is Financed Emissions, which are mostly lending-based for banks.

PCAF Part C is Insurance-Associated Emissions (vehicles and commercial)

Yet, PCAF Part B, focused on Facilitated Emissions or the ones that investors need to claim, which is again the group responsible for kicking off this pressure of The Great Disclosening, remained unreleased.

I’ve been watching PCAF for a while now. This has been the website graphic throughout the year and still appears today.

In July, there was a brief blink-and-you’ll-miss-it article from Quartz proclaiming Banks seek to dilute accounting standards for carbon emissions. At stake was the amount of emissions firms had to disclose or ‘weighting.’ On the table were percentages ranging from 17% to 33% to 100%. Of course, activists were pushing for 100%, but the PCAF board launched the standard last week with a 33% recommendation, meaning that firms can effectively disclose a third of their emissions.

Strangely, the graphic above remains on the site’s homepage (as of 12/4/23), but the PCAF Part B standard is available online.

Context, Methodology, and Weighting Matter

On the surface, the 33% news is pretty disappointing for activists. However, little hope can be found by understanding the context, methodology, and weighting.

PCAF favors financed emissions as the leading influencer of emissions ownership in the financial sector. In other words, lending and financing activities more directly influence the ownership of emissions by the banks for Scope 3, Category 15. Logically, this makes sense because borrowing leads to activities that otherwise wouldn’t have been generated downstream.

However, context from the standard explains how the 33% was arrived at. We must sidestep to visit another organization, The Basel Committee on Banking Supervision (BCBS). Basel is the primary global standard setter for regulating banks and has compared debt and equity instruments (or capital markets) to lending (from banks).

…underwriting (leading to facilitated emissions) is only ~17% as impactful as balance sheet exposures (leading to financed emissions).

However, Basel is mindful that this can change over time because:

Earlier in 2018, the Basel approach weighted balance sheet exposures as only three times more consequential than underwriting, specifically ~33% as impactful as balance sheet exposures.

So, that is the context of the 17% and 33% weighting factors. Lest activists believe that firms can now hide their facilitation; the methodology has two things to note. First, firms may decide not to apply the weighting factor of 33% and report 100% of facilitated emissions. Second, firms must report on the emissions and the weighting factor used. So, activists can still figure out the total emissions with some math.

Ultimately, showing improvements remains unaffected as the reporting firm should use consistent weighting across transactions, but the word should is a little too squishy for me. A risk could be that this could allow heavy-emitting transactions to follow the 33% weighting, with low-emitting transactions hitting the 100% weight. This blend of weighting would be nearly useless and indecipherable.

Does PCAF Part B Matter?

Scope 3, Category 15 is wildly complex for banks and capital markets firms because it relies on the firm to know the emissions around the borrower (PCAF Part A) or the transaction (PCAF Part B). This is addressed right in the Executive Summary, however.

Limited data is often the main challenge in calculating facilitated emissions; however, data limitations should not deter financial institutions from starting their GHG accounting journeys.

Despite the availability of data, PCAF Part B matters very much. The Executive Summary states its importance as follows:

Until now, there has not been a globally accepted standard for measuring and reporting emissions associated with capital market activities.

This is VERY true, but we must go deeper into why it matters.

Revisiting Larry Fink, banks and capital markets firms are the ones that started The Great Disclosening and the push for comparable data, leading to new standards and regulations. As I’ve written, these firms chase comparable data to assess their financing and facilitated activities. This way, lenders and investors are the primary stakeholders of sovereign, corporate, and project ESG data.

Until now, these firms have had no comparable way to communicate their most material emissions contributors to stakeholders! When a bank or capital markets firm reports data, I believe the public is the primary stakeholder of the data, giving us visibility into the activities and influence of capital to do what Larry Fink wrote about back in his 2018 CEO letter.

Society is demanding that companies, both public and private, serve a social purpose. To prosper over time, every company must not only deliver financial performance, but also show how it makes a positive contribution to society.

Financial services firms are companies, too, after all. Therefore, PCAF Part B is vital because we should now see how capital markets leverage the ESG data they’ve been clamoring for to do what they want everyone else to do.

Yet, did this standard come too late? This week, the Financial Times’ Big Read was called The Real Impact of the ESG Backlash, which wraps with a bond fund manager predicting that ESG will be dead in five years. The timing of this statement against the disclosures finally being available for the industry that started the ESG data race is hysterically timed.

More seriously, there is considerable caution at this crucial point if ESG does last.

Like any disclosure, we need more than the metrics and weighting of PCAF Part B. Stakeholders need transparency into strategies to make sense of the numbers. So, the question, as always, is this:

What are these firms doing to support a sustainable and just transition?

That question, unfortunately, isn’t answered in the metrics, but the data is the proof of their story. While it is fitting that disclosures (and accountability) have finally come home to roost, we need action to progress.