ESG: Finding clarity back at the start

It's been almost 20 years, but ESG's intent is lost in opportunistic activity

ESG can’t win. It finds itself at the intersection of two opposing yet bizarrely aligned forces. Thanks to Larry Fink’s annual CEO letters (primarily from 2018 and 2019) and a series of unfortunate events starting in 2020, ESG is under fire from two extremes, with companies, asset managers, and regulators stuck in the middle.

On one side, we have conservative political leaders who incorrectly believe that ESG is pushing a liberal agenda. There are groups, like the State Financial Officers Foundation proclaiming they are “educating Americans on the dangers of ESG” as if

There’s a secret liberal cabal trying to force you to save the world with your hard-earned money.

Saving the planet and creating equity for all goes against your personal freedom.

I have no patience for these people, but legitimate confusion exists. Financial services firms must get their collective act together and better define ESG and Sustainable Investing.

On the other side, we have activist investors who have heard the acronym “ESG” and made assumptions that it would save the world based on confusing messaging from those selling financial products. I recently signed up for TikTok to see what the narrative is out there. Activists incorrectly frame ESG on the platform as a way to vote your values with your dollars, but that isn’t it either.

ESG won’t save the world, nor was it ever meant to. There are ways to invest your dollars to save the planet, but it is through Impact Investing or other thematic vehicles. Some companies are good at understanding the ever-changing world and its impact on their operations while working to save it. This lack of a black-and-white perspective makes ESG a challenging topic to understand and, like everything, abhors a catchy sound bite.

And so, without clear regulations and definitions, ESG has been left open to interpretation and wielded opportunistically to create new financial products with little clarity or transparency.

Both opposing sides echo a common refrain, however. It seems no one has clarity on what their money is doing. Conservatives worry their constituents’ funds are driving dollars away from their state’s sources of income (oil, gas, coal, etc.), and activists believe that their dollars are going to save the planet or social causes but are waking up to the reality that ESG Investing doesn’t do that.

Both concerns are legitimate, but neither has to do with ESG.

ESG was first defined in the UN Global Compact’s whitepaper “Who Cares Wins.” Still, I rarely see the whitepaper referred to whenever it’s defined in the media (which, unless written by a practitioner, is usually way off and contributes to the confusion) or when discussing the controversies around it.

After talking with Witold Henisz on NPR’s Up First about the risks of political blowback, Micheal Copley explained how ESG supporters are responding:

They think that if ESG is explained in concrete terms, voters will see it as a reasonable way to approach investing. They are also trying to show that these attacks are part of a long running effort to keep the US from dealing with climate change.

This is pretty accurate and one reason I started this newsletter. So, let’s go back to the start and revisit the original whitepaper to see what guidance it could give to reframing the current social narratives.

What is ESG as defined by the UN Global Compact?

The framing in the introduction of the whitepaper sets ESG apart as “issues which have or could have a material impact on investment value.” (page 2). Right before that statement is how it should be differentiated from the things conservatives are now concerned about (ie. ‘woke’):

Throughout this report we have refrained from using terms such as sustainability, corporate citizenship, etc., in order to avoid misunderstandings deriving from different interpretations of these terms. We have preferred to spell out the environmental, social and governance issues which are the topic of this report.

The UN Global Compact saw the opportunity for conflation by interpreting sweeping terms early on, but it was ultimately unavoidable. Since this was written, there has been an opportunistic capitalization on the fine line between ESG and these other topics. Many financial services firms and corporates have used platitudes and flowery language to blur the lines between good corporate citizenship and risks/opportunities.

While a company can address Environmental, Social, or Corporate Governance challenges, ESG issues are material risks and opportunities.

Are there examples given?

Finding broad material issues for every business is a challenge, but the UN Global Compact provides some pretty decent ones:

While specific examples aren’t given, let’s unpack one issue from each area with a modern example to illustrate the point.

Environmental issue: Climate change and related risks

Issue: Hurricane Ian caused between $35 billion and $55 billion of insured claims, making it one of the costliest natural catastrophes ever.

Example: Insurance rates in Florida and other parts of the world with extreme weather will increase due to global reinsurance increases or lack of availability (source).

Social issue: Community Relations

Issue: COVID has kept people inside for entertainment instead of seeking more social options. Some theaters, most recently the San Marco, have closed.

Example: What is a risk for theaters has turned into an opportunity for streaming services (source, source).

Corporate governance issue: Management of corruption and bribery issues

Issue: Poor business practices can lead to fines and reputational risk.

Example: Honeywell was investigated by the SEC for bribery issues a decade ago, but was just fined $81 million in 2022 (source).

These examples are straightforward, but conflation comes from the fourth environmental bullet and the fifth social one in the list, which are identical.

There is a reputational risk when ignoring even the non-material ESG issues. For example, this could lead to consumers choosing an eco-conscious brand or talent shifting away to a more purposeful job (check ClimateBase to see what I mean). Companies need to do it all, which is why I often write about ESG and these other CSR-type issues.

It is also important to note that just because your company pays attention to one ESG issue in one pillar doesn’t mean you have solved that particular ESG challenge. These issues are complex and often require companies to look across the other letters for additional context. In the insurance example above, what does a lack of insurance mean for low-income communities who don’t have the flexibility to afford higher rates or move?

What’s the logic behind ESG?

Managing a company well means understanding these complex, multi-faceted issues. On page 9, we find why investors will care and why all stakeholders should care.

Companies with better ESG performance can increase shareholder value by better managing risks related to emerging ESG issues, by anticipating regulatory changes or consumer trends, and by accessing new markets or reducing costs. Instead of focusing on single issues, successful companies have learned to manage the entire range of ESG issues relevant to their business, thereby achieving the best results in terms of value creation. Moreover, ESG issues can have a strong impact on reputation and brands, an increasingly important part of company value. It is not uncommon that intangible assets, including reputation and brands, represent over two-thirds of total market value of a listed company. It is likely that ESG issues will have an even greater impact on companies’ competitiveness and financial performance in the future.

In other words, if you work, buy from, or do business with a particular company, you should care about how they manage their ESG issues because it helps ensure that they can be successful and thus stay in business. A company should care because ESG is at the core of value creation at best and maintains intangible value via reputation at worst. This isn’t a perfect idea, and there is another debate about whether ESG is tied to growth (here, meaning short-term growth, which we’ll get into below), but it doesn’t have to be. Instead, consider an included quote from Jean Frijns, who was the Chief Investment Officer for ABP in 2004:

There is a growing body of empirical evidence that companies which manage environmental, social and governance risks most effectively tend to deliver better risk-adjusted financial performance than their industry peers.

Taking action around ESG issues can improve a company’s risk profile. Logically, that means they should be better protected from risk. Of course, as illustrated in the previous section, you must deal with your business holistically across all risk areas, not just one particular pillar, as risk can come from anywhere.

What did the UN Global Compact say about oil and gas divestment?

A common refrain from conservatives is that ESG will lead to a massive disruption to energy markets. On the other hand, activists worry that ESG isn’t doing enough to punish oil and gas companies. Again, ESG isn’t trying to do either.

The word ‘divestment’ doesn’t appear in the paper, and this is years before ‘cancel culture’ and ‘woke', so let’s not even go there. The paper also doesn’t cover our current climate crisis directly but points to the risk it presents.

NOTE: I have personal opinions on this last point (ie. we need to save the planet), but again, it is hard. We can’t, for example, prevent emerging markets from quickly growing under fossil fuels. We can, however, find new ways to fund their green transition while doing the same.

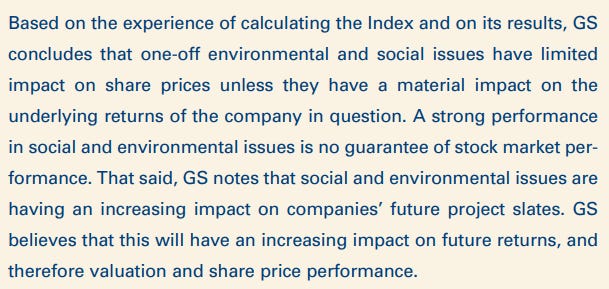

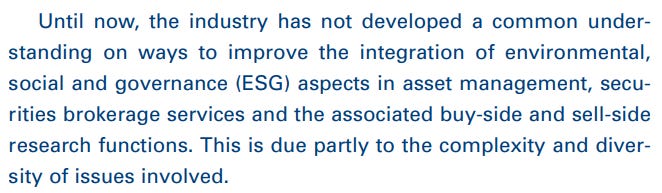

As if the UN Global Compact could predict this issue, they cite a Goldman Sachs study on oil and gas on pages 13-16. There are two snippets worth considering:

Goldman Sachs concluded that these issues don’t impact stock price unless they have a material impact. Long-term future returns are called out, which pension funds, like those in conservative states, let’s say, focus on. Still, many firms and investors focus on the short term in our world of quarterly financial reporting.

It’s worth noting that earlier in the report, there is a note about the World Economic Forum’s opinion on this matter. “Intangible aspects related to ESG issues play an increasingly important role in value creation but that analysts’ short-term focus hinders them in recognising this trend.” It isn’t just analysts. We’re all wired to think this way because that is how the markets operate. For example, salary increases occur annually, and employability often hinges on short-term company performance.

Interestingly, Goldman Sachs noted the vision for a low-carbon world and its value (ie. we need to transition, and a good management team would understand that). There is a little bit of a passive/aggressive information relay to companies in the next paragraph, stating that:

Still, nothing about divestment, but we can see that the low-carbon world was already on the minds of financial services firms for the energy industry back in 2004. This shouldn't be a surprise for an energy company with good governance practices, but as we all know, the pressure to maintain the status quo has been high from energy lobbyists. Frankly, this is some type of governance, but not one I’d label ‘quality’ or ‘good’ when considering the pace at which the world is trying to move away from fossil fuels.

Where has ESG gone awry?

And so, with the long-term view and the low-carbon world in mind, there is a lot of conflation in the financial markets between what ESG is and what it isn’t, despite this hopeful statement early on in the report.

This challenge was never resolved but accelerated around the hard pivot in 2020 to ESG and the subsequent pressure from stakeholders to address table-stakes issues like sustainability (carbon mostly), diversity/equity/inclusion, and other CSR issues. Companies must be doing it all, but many are missing one side or the other or are not effectively communicating what they are doing. Investors want a range of things, but with how close material and non-material issues are, financial services products are mired in confusion. As a result, it is still unclear today what is being prioritized from the markets to companies regarding ESG Investing or Impact Investing. For example, Telsa might go out of the S&P ESG Index for their poor attention to S and G issues (ESG) yet remain in a fund focused on the environment (Impact).

This is partly because companies can’t tell what investors are trying to create around a financial product. This is the ultimate irony of ESG as firms bemoan the lack of quality data, but companies can’t figure out what data to report, ESG or CSR disclosures. For example, in talking with a company about their supplier carbon disclosure problem, I asked what they were doing about climate risk for their facilities. The question came back, “Investors don’t care about that (pause), do they?”

Who knows? I would think an ESG investor would since that is material, but an Impact investor may not. Should the company report on both? I believe so!

This statement from the whitepaper is just as relevant then as it is today:

Fund managers and analysts, on the other hand, when asked if they are satisfied with the information they receive from companies answer “No” by a wide majority of over 55%. Something is clearly not working in the communication between companies and financial markets on these issues.

With many ways to create financial products and high demand, firms want all kinds of information, including material ESG and non-material E, S, and G data. New perspectives like double materiality are also gaining interest. This is the impact of the company on the world (ESG) and the impact of the world on the company (sustainability). And so, the problem is the same one we started with. It is rare to find clear communication on how an investor’s money is being used, leaving companies, investors, and stakeholders asking, “Is it ESG or something else?”

One lingering thing that bothers me is that active ESG education doesn’t appear in the whitepaper except for the communication between companies and financial services firms, mostly through the existing lens of Investor Relations teams focused on the matter. Board education on ESG considerations is completely absent in the whitepaper, which might be one reason for the confusion and conflation.

Consistency would go a long way. Companies should be able to always believe that ESG investors interested in risk would care about climate risk and Impact investors would care about thematic issues like sustainability. Unfortunately, a financial services firm might create an ESG product but focus on sustainability instead. On the other hand, they might create a green fund that looks at risk instead of global impact. Inconsistency breeds controversy, and if firms can’t get their act together by the time they show up to Congress, progress will slow.

If we’re truly to move forward with ESG, it’s time to revisit this whitepaper with the intent to clearly define these terms alongside a plan to educate stakeholders. The result should be better quality data from companies, which financial services firms want, more satisfied investors who can confidently invest their money in products, and fewer controversies around managing risk.