Followers: Another goal in the wall

Part 1 about the type of companies and efforts pulling away from ESG

Welcome to Part I in a three-part series on the types of companies and efforts pulling away from ESG. Each one will follow a similar structure to see what we can learn. As they are published, I will update these posts with links to the other parts. Enjoy!

If you randomly sampled the past three months’ worth of ESG-related news, you might find many articles that cover the various pullbacks. If you further lumped them all together, which is how our brains work in today’s constant ‘always on’ world, you might think that conservative anti-ESG efforts were working, or you might conclude that companies are ‘getting back to business.’

The reality is much more nuanced, and if there is one thing that people who understand ESG thrive on, it is the nuance of this topic.

After writing about the anti-ESG crusade’s recent successes last week, I realized I may have done you a disservice. There is more to what is going on out there, and at least three categories of companies are currently in motion around ESG restructuring.

A couple of ground rules before we get into this:

It is essential to recognize that activists are pushing and pulling around ESG, trying to refocus companies to do more or less. In both cases, neither may be engaged in ESG, stakeholders, or materiality, and both may swing too hard toward values to drive impact.

The slowdown in institutional investors’ support of ESG proxy resolutions will not be covered here. Still, I believe they are doing their clients a disservice by not diving deep into nuances like these and the resolutions that arise.

When reading about these companies, I encourage you to go deeper and read the surrounding information. For example, what is in the company’s ESG report, 10K, or their industry news? Not only are companies not getting ESG right all the time, but the media is getting it wrong. Just as you approach any article with a healthy dose of skepticism, do that with ESG articles. After all, I don’t always get it right or complete!

As with many articles focused on a singular perspective, companies have many nuances and likely don’t fit neatly into the categories I have observed. We will see this throughout. I'll lead with balanced examples for this article and the next two as much as possible.

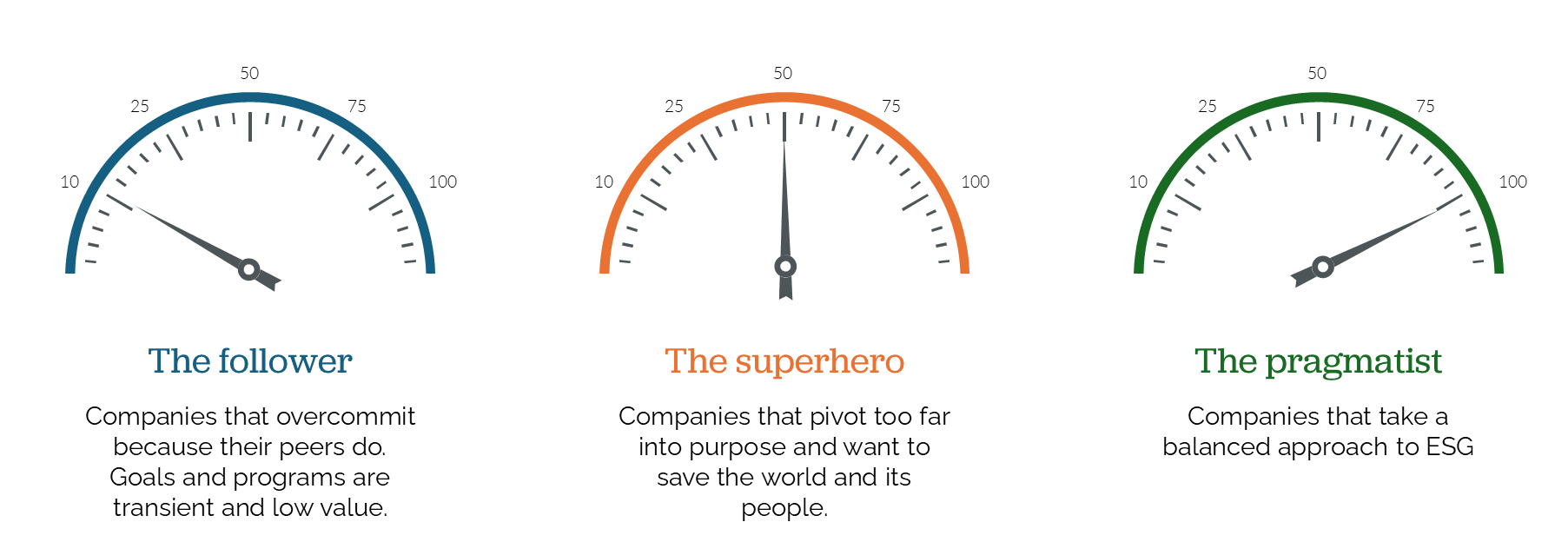

The three types of companies

So, in all of this agita, I believe three types of companies are restructuring their ESG and ESG-related programs.

The follower is a company doing the bare minimum to comply with emerging regulations. It likely has spun up a range of ESG-related programs post-2020 in the face of stakeholder pressure. They’ve examined their competitors and tried to match programs rather than examine stakeholders and materiality. This type of company is an easy target for anti-ESG talking points as the public-facing programs are often not material and are of low company or systemic value.

The superhero is a company that wants to save the world and its people. This company may or may not have the luxury of doing so, based on its ability to fund programs and stakeholder appetite. Materiality may or may not be a consideration in these programs as they lead with ‘ideal’ ESG-related values.

The pragmatist is a company that takes a balanced approach to ESG and either recognizes the risks and opportunities or approaches them through a business perspective.

Each group doesn’t exist in a silo, but I believe that companies skew into one of these categories. As we’ll see here, we may have followers who back away from their goals but have a clear vision for the long term. We may have superheroes who pivot into pragmatism or pragmatists with a mix of focus from the other two. Companies may even be followers in one pillar of ESG and pragmatists in others.

Let’s make this real with examples of companies appearing to be followers in one area and doing other types of work.

The follower

The follower sits in the group I wrote about last week. These companies are engaging in net zero goals without carbon being a material issue simply because everyone is doing it (although you could say that about most companies). They also spun up transient DEI goals without much thought to stakeholder integration and have likely fired their Chief Impact or DEI officer in the past 18 months. These companies also follow ESG and ESG-related programs because their peers are.

Let’s examine a company that appears to be in the follower category if you only look at the latest news while recognizing its material intersection of ESG like a pragmatist.

John Deere is an agricultural and heavy machinery manufacturer. I’ve had a consumer-grade John Deere tractor that lasted about 20 years, and I just bought my second one. If you’ve been with me in an online meeting, you might have seen my John Deere mug, one of my favorites.

Like many companies, John Deere may have over-pivoted in the Social category by going beyond stakeholder support at the intersection of its company into broad support for a wide range of activities not core to its business.

In July 2024, the company backed away, as many did, due to conservative pressure. In a statement released on X.com, the company stated that it is backing away from sponsoring external events and non-professional Employee Resource Groups (ERGs) while reassessing internal training efforts. To be clear, John Deere restates this: they’ve never had diversity quotas and are committed to a diverse workforce. You can still find their stakeholder approach on their website.

In its 2023 10K, John Deere includes many of these programs in a section under Human Capital on Diversity, Equity, and Inclusion. It will be interesting to see how this section is managed in its 2024 10K, published after the statement on X.com. The Human Capital section has many other relevant ESG intersections, including ethics, health and safety, compensation, training, and human rights. All of these are also material Social issues.

They recognize Social issues further under their Strategic Risks section in this statement.

We may be unable to manage increasing political, economic, and social uncertainty in certain regions of the world, which could significantly change the dynamics of our competition, customer base, and product offerings globally.

So, we might have a case where the company followed in one specific area while still monitoring material social issues.

Along the Environmental pillar, John Deere didn’t follow along with others with a future net zero goal. In their latest 10K, the company recognizes the reputational management piece of such a goal, which is what trips up most followers.

…customer preferences in the markets we serve are changing as a result of ongoing social and regulatory focus on sustainability as these markets transition to less carbon-intensive business models.

Yet, the company quickly moves into a sustainability issue for stakeholders at the material intersection of its business.

The development of alternative farming techniques, carbon sequestration technologies, and new low-carbon biofuels are changing farmers’ business models and equipment needs.

What immediately follows that second point is this.

If we fail to continue to develop or invest in emerging technologies to meet changing customer demands, we will be at risk of losing potential sources of revenue, which could affect our future financial results.

Again, one company may make more pragmatic strides in a particular area.

Following the goals or the ESG issues

Moving on from John Deere, there is a significant trend to recognize here. Companies will set goals or join ESG-related coalitions around capturing a reputational opportunity. As their bright-eyes sustainability offices (because this usually happens along the Environmental pillar) attempt to tackle the challenges, they find the goals were set arbitrarily or that the challenge is much higher than anticipated.

For example, in July 2021, Crocs announced a goal to reach net zero by 2030. Two years later, that goal was pushed back to 2040. Several factors caused this, including acquiring HeyDude and the company’s overall revenue growth. In their last three Comfort Reports, there is a mention of the company having completed a materiality matrix and updating it to a double materiality matrix in 2024, but it is not shared. I am really curious about how material carbon emissions are against other factors. I’d weigh it somewhere in the middle; their footwear relies on fossil fuels, similar to LEGO’s core product.

The Crocs report mentions fossil fuels only three times. All relate to sourcing materials, but one is tied to a particular goal.

In 2023, we increased the amount of bio-circular content in our Croslite™ compounds to 17.3% on a mass balance, annual average basis and we have a goal to achieve 50% bio-circular content in our Croslite™ compounds by 2030. This raw material diversification reduces our reliance on fossil fuels, increases resilience across the supply chain, and addresses investor and customer expectations.

While decarbonization and a responsible energy transition are essential for our survival, getting there requires more granular goals like this.

In these specific and material goals, a company will make an impact as only it can.

For followers or those engaging in following efforts, this is an excellent example of taking a reputational-based goal and turning it into something actionable and pragmatic. Specifically, working on the compounds in their materials is trackable and could capture both material and reputational benefits.

Crocs also mentions setting SBTi-aligned goals. Many companies are trying to figure out how best to manage this, and it is becoming more of a reputational risk than a material progression. For example, when SBTi drops companies, it becomes a splashy news story, engaging in a cycle to shame the company. SBTi goals also show up more often in RFPs.

The one thing SBTi misses appears to be the material intersection of carbon with a company. The SBTi guidance understands material carbon vs. immaterial, but materiality across all issues, not just one, is missing here. In other words, taking a science-based approach to the realities of decarbonization is aspirational and can help set the company on one path. Like any net zero commitment, that path may not stick if the plan does not adequately consider the realities of business operations or trade-offs in other areas over time.

While SBTi is not a trap, thinking that your company can set these goals without considering your business or other pillars of ESG is a trap. Again, it will fall over with the slightest nudge.

What followers can do

Followers who have overcommitted or find efforts that fall into the follower category have a unique opportunity to reset and manage their reputational risks while doing so.

It starts with understanding your material ESG connections and stakeholders. From this point, everything you do is business-relevant and not outside of it. This builds defensibility.

Recognize that carbon and DEI may not be your most material issues, but they should probably be in the mix somewhere because, chances are, they intersect with your business at least somewhere. Still, are there other Environmental areas where you could lead? Can you attract talent or customers with a different type of approach? Grappling with where your connections are is the first step in setting a strategy to address the issues and chase the opportunities.

And if you are good at running your business, use existing mechanisms to mainstream and incentivize accordingly.

Followers should take comfort in this: The message that your company has done the work to set appropriate ESG goals for your business is worth more than an arbitrary goal set in a far-off timeline. This is what stakeholders will appreciate if communicated effectively.