While I am a self-proclaimed ESG Advocate, I think that my perspectives, even on ESG topics, aren’t so limited to not understanding others. As a result, I think some of you might be surprised by my view on Berkshire Hathaway and the recent Annual General Meeting (AGM). It is worth noting that I own no stock in Berkshire Hathaway unless it’s buried in my 401k.

Just recently, I was chatting with someone about ESG, and they rightfully challenged me with, “Well, Warren Buffett doesn’t like it.” On the surface, this appears to be the case. My initial response was, “You know you’re right, but I also don’t hear that very often,” and it’s true. Thinking through my years of conversations about ESG, Buffett rarely comes up, but even Bing Chat believes the highly successful Oracle of Omaha does not appear to be a fan of ESG.

Warren Buffet is a liberal and a Democrat but he is not a fan of ESG. He has even opposed proposals for annual reports on climate change and diversity initiatives. His stance is running counter to Wall Street’s expectations given the growing attractiveness of investing in sustainable ventures.

Still, I never really dug into what Buffett said about ESG and, like many, relied on the headlines. So in searching for his opinion on ESG, there is little direct information but much analysis, which is all I will do here. Still, I think the commentary out there misses the point.

ESG might run counter to Berkshire’s Governance model

Managing an ESG program from the position of a holding company is no small effort. These conglomerates must navigate and aggregate multi-national regulations, disclosures, materiality, stakeholder analysis, and company project work into a single view. I’ve seen similar models in Private Equity, but they leverage well-established engagement models. This work represents a heavy lift for a conglomerate starting from scratch.

Broadly speaking, Berkshire Hathaway runs a Governance model that includes three key points:

Companies only report what is critical to the holding company.

The company appreciates that shareholders trust them with their money.

As we all know, ESG requires a lot of data and reporting. For example, in this 2021 Forbes piece, it is noted that Buffet is the only S&P 500 CEO who doesn’t receive an income statement. It is also stated that “Berkshire does provide substantial disclosure in its shareholder reporting.” I wonder if he doesn’t see value in forcing his companies to generate any reports, ESG or otherwise.

On the other hand, he called ESG-type reports and activities “asinine” as well, but I don’t think the reason is clear if it is because he doesn’t see the value or doesn’t like reporting. Frankly, it might be neither. Whatever Buffet has been doing to grow the wealth of the people who trust him with their money has been working from a returns perspective, with or without ESG.

Now, those are just recent statements around reporting that provide little clarity. However, if we go back to 2019, we find this Buffett quote in the Financial Times:

If they asked [the fund directors], ‘Do you want the board of directors and the managers of your companies to spend time and energy on environmental, social, and governance issues or do you want them to spend all of their time and energy on increasing the value of your share?’, I’m rather sure that an overwhelming number of them would choose the latter.

Frankly, I don’t see anything anti-ESG in this statement. If ESG is focused on material risks and opportunities and long-term growth, then wouldn’t companies looking at ESG concentrate on increasing the value of shares anyway? Underpinning this quote might be the conflation of non-material issues with ESG because, as always, ESG is in the eye of the beholder. Perhaps he is referring to the borderline win-win or ‘do well by doing good’ sentiment here. Regardless, if an issue impacts the value of the share, it seems like Berkshire Hathaway’s companies would focus on it, ESG or not.

Still, this past weekend was the AGM, so let’s look at the six shareholder proposals and remember a couple of things. First, Berkshire Hathaway has a successful Governance model, as evidenced by its longevity and returns. Second, even if it isn’t perfect, no company is. Third, the companies owned by Berkshire Hathaway do have DEI statements and CSR reports, and some even align with the Science-Based Targets Initiative. The sustainability reports for those companies are centrally listed here. Fourth, remember that Berkshire Hathaway is not aggregating that information in a single report, nor are they interested in doing so.

Five ESG proposals and one anti-ESG proposal

The news (and OMG Twitter, please stop) reported that there were six ESG proposals on the table for the AGM, but it was actually five proposals related to ESG and one anti-ESG proposal. Before diving in, you can check all six proposals at Business Insider (including Berkshire’s responses) or the two key Environmental and Social proposals at As You Sow’s Resolution Tracker.

Proposals 1, 2, and 3: Shareholders are looking for information on Berkshire’s financed emissions (Scope 3, Category 15), but there is also a callout here that Berkshire is the only insurer not sharing information on its climate risk. The proposals ask for pretty standard reporting, including annual reports, the company’s physical and transitional climate-related risks and opportunities, and how climate risks are governed by the company (G). There are also questions about how the company plans to help measure and reduce emissions to align with the Paris Climate Agreement (sustainability).

Status: Rejected 3-to-1.

The first proposals here concern climate change, sustainability, and ESG. Here, we see the requirements to report that Buffett isn’t convinced about (and I agreed in The Great Disclosening last week). While disclosures are essential for action, I’m not convinced that Berkshire Hathaway should be the one doing it. Instead, individual companies should have this burden, again based on the Governance model. Again, this is a theme across many of the company’s responses.

The better question for activists might be this: How do I convince Berkshire Hathaway to funnel its $130B of cash toward sustainable project work? I don’t see that happening, but it’s nice to dream.

However, to the following few points, understanding the company’s overall climate and transitional risk, including exposure to insurance constraints under extreme weather, is a material ask. Yet, in 2014, Buffett said this:

I don’t think in making an investment decision on Berkshire Hathaway, or most companies — virtually all of the companies I can think of — that climate change should be a factor in the decision-making process.

That was nine years ago and the clearest callout against an ESG issue. However, I’m confident that the effects of climate change, especially for the insurance industry, have evolved, and insurers may not be ready. So again, this is a material risk.

The question for me is where should this fall, at Berkshire Hathaway’s top level or each company’s executive level? Since Berkshire leverages a highly decentralized management model that gives companies operational independence, it would seem that deference to those executive teams would be best. After all, this is a unique Governance model that appears to be working. Attention here would prove that model works.

Proposal 4: That Berkshire Hathaway reports quantitative data on the effectiveness of the company's diversity, equity, and inclusion efforts.

Status: Rejected 10-to-1.

When reporting DEI data, companies in the US already confidentially collect and report their EEO-1 data to the US Department of Labor (DOL). In other words, part of this proposal asks more companies to publish the already collected EEO-1 information, as 94% of the S&P 500 companies do (per As You Sow). However, only one out of the 63 companies publishes this (as of November 2022, Kraft-Heinz).

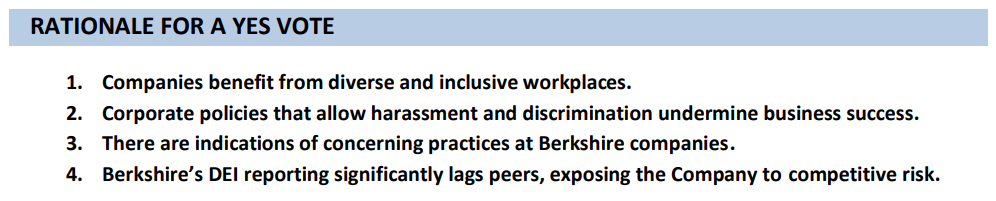

Per an excellent As You Sow report on the proposal, the rationale for a ‘yes’ on this vote aligns with four points.

The first two are tied to well-documented research, and we’ve already covered the fourth bullet, reporting. Still, that third one is worth a look. The report lists three specific examples of discrimination across three Berkshire Hathaway companies. These Social risks must be managed, as they can result in fines and reputational issues. However, it is difficult to tell whether these are single companies' one-off or systemic issues across the conglomerate. Of course, to understand that, you’d have to investigate it from the top down, which is what the proposal is asking for.

Still, I believe the rejection here is less due to reporting burden since the US companies are already required to report to the US DOL and more to do with the decentralization and the requirement to analyze the data in return for a perceived low value. It is worth noting that in spot-checking some owned companies, DEI appears to be more touted than sustainability on their websites. This doesn’t mean DEI is well in hand, but metrics don’t prove that out either, necessarily.

Proposal 5: Berkshire separates the CEO and Chairman roles, resulting in Buffett stepping down as Chairman.

This is a common ask for companies where the CEO and Chairman are the same. The consolidation of power and influence is a considerable risk typically. Buffett holds a lot of control in these positions. Still, I believe Berkshire Hathaway’s existing Governance model ultimately outweighs the risks underneath this proposal.

Proposal 6: That Berkshire Hathaway receives a commitment that its portfolio companies avoid supporting or taking a public position on any controversial social or political issues.

Status: Rejected at 99%! 👀

And here we have an anti-ESG proposal, which was also very soundly rejected. This one was proposed by the American Conservative Values ETF, which sums up its stance as follows:

…based on the conviction that politically active companies negatively impact their shareholder returns, as well as support issues and causes that conflict with conservative political ideals, beliefs, and values.

I agree with this first half, which might surprise readers. Companies should focus on material systemic Environmental and Social issues, not necessarily wading into every political issue. But, there is a lot of gray area here. For example, for a company that wants to support its employee stakeholders, supporting women’s health rights is likely a place to wade in. But on the other hand, supporting gun reform or rolling back the death penalty are issues that are likely less material broadly.

I must disagree with the second half of that statement, as this appears to be a far-right dig at ESG issues without much substance. In other words, it is a values-based argument against something that doesn’t always have values aligned. I’ve seen flavors of this be rejected at other companies. Proposals that go against an ill-defined ‘controversy’ will likely always fail, especially at a conglomerate that does not dictate policy from the top down.

One last thing on sustainability and ESG at Berkshire Hathaway…

And so, the initial perception in seeing these proposals struck down might be to believe that Buffett doesn’t like ESG, but I’m not convinced that is the case in the context of its Governance model. Here’s some information that leads me to believe it’s less about ESG and more about Governance.

Berkshire Hathaway appears to have collected their shared sustainability and ESG knowledge into a Sustainability Leadership Council across its portfolio.

The bullets in this list give me hope as long as they are more than bullets on a slide. It reminds me of the collaboration in Private Equity and across ESG-focused VCs. There is a collective knowledge that can be used to help manage ESG issues by sharing lessons learned. I leave it to you to determine if this is more meaningful than aggregating disclosures, as there is little information online about this effort or the sustainability summits.

A few weeks ago, I covered Governance’s role in SVB’s downfall and mentioned that it is the one pillar that could take a company down and is often overlooked (Teaser: I’ll be on The ESG Talk Podcast this Friday, talking about Governance). While the AGM may be disappointing for those looking for progress, Berkshire Hathaway’s rejection of these shareholder proposals appears to be a Governance call, but they seem to be doing something.

Yet, there might come a day when shareholders finally push through the wall to initiate these changes. After all, just because Governance is working today doesn’t mean it is perfect or will remain steady. If that happens, management dynamics across the portfolio of companies will have to shift, introducing a potential new Governance risk in its wake.