Overseeing ESG means defining it

The US House Oversight Committee hearing on ESG points some big problems

For a while now, you could sense that ESG was heading to a US Congressional hearing. While every other country seems to think ESG is an additive perspective, conservative US politicians have latched onto ESG as a recent target, with a call of “woke” leading the charge.

This pressure culminated in last week’s House Oversight Committee hearing on ESG, Part I, also titled the Hearing on Damaging ESG Practices with Attorneys General. The House Majority witnesses were two conservative State Attorney Generals. In attendance from Utah was Sean Reyes, and from Alabama, Steve Marshall. It is worth noting that Governors from both states signed Florida Governor Ron DeSantis’s anti-ESG letter.

Meanwhile, the House Minority witness was Illinois State Treasurer Michael Frerichs. Frerichs’s office manages $52B of funds across state funds, college savings, and other state and local investments. He is also a trustee on the Illinois State Board of Investment, which manages $28B in pension funds.

Of note, no asset managers or companies were harmed during the filming of the session because they weren’t invited.

What was the ESG hearing about?

Stripping away the political rhetoric, the issue on the table at its most basic level ‘appears’ to be this:

Should state pensions consider ESG as part of an investment strategy?

Remember, this is one investment area that states and their politicians can directly control. Each state maintains its pensions and works with asset managers to manage the investments on behalf of pensioners. In effect, they are the custodians of their citizen’s long-term savings.

I write ‘appears’ because this hearing was all over the place, which was unsurprising. From the public’s perception to political ambition to corporate change through financial services firms’ opportunities, ESG is an ill-defined term, full of nuance and complexity. So let’s define it using the three terms the committee and respondents used:

ESG Investing: Investors may assess material E, S, and G risks and opportunities to drive long-term growth. For example, climate risk, stakeholder risk, and board management principles can all impact the company’s ability to deliver returns consistently.

ESG issues not universally material, such as the transition risk to clean energy, may also intersect here, which was a key talking point.

There is additional complexity here as ESG is mostly a value-based exercise, but values can enter into the mix at the intersection of stakeholders. For example, a company may support women’s healthcare around issues like abortion to support their employees and retain talent, which is a material issue.Socially Responsible (SRI) or Responsible Investing: This investment strategy is where an investor moves capital towards a social good aligned with their values. For example, an environmental activist may divest from fossil fuels and invest in high-tech renewables.

As with ESG investing, sometimes these issues can be material, which causes a lot of conflation. For example, an SRI investor may believe that the fossil fuel model does not have long-term value due to changing corporate perspectives.

There were a couple of bright spots in the hearing where ESG Investing was accurately described, primarily by liberal committee members (but not all) and, as you might expect, Frerichs, who pointed this out:

Most people don’t know what ESG is. ESG is data. ESG is simply additional information that investment professionals use to assess risk and return prospects. It is about value, not about values.

In order to maximize returns, an investor must be able to manage and mitigate risk. The more data we, as investors, have, the better informed our decisions are.

Is ESG a part of fiduciary responsibility?

Much of the talking points centered around the definition of fiduciary and its intersection with ESG. So, let’s build our perspective with another definition, pulled straight from The US Department of Labor (DOL) website about The Employee Retirement Income Security Act (ERISA), which came up six times.

The primary responsibility of fiduciaries is to run the plan solely in the interest of participants and beneficiaries and for the exclusive purpose of providing benefits and paying plan expenses. Fiduciaries must act prudently and must diversify the plan's investments in order to minimize the risk of large losses. In addition, they must follow the terms of plan documents to the extent that the plan terms are consistent with ERISA.

We know (because I wrote it above) that ESG Investing focuses on long-term growth by managing material issues, which can help inform investment decisions. For example, higher quality decisions might ensure ERISA’s benefits and payout of plan expenses. Of course, no investment is ever a guarantee since no company is going to get everything right all of the time. Still, the idea is that ESG might help an investor or company uncover and manage risks, making it a fiduciary responsibility.

In the current debate around ESG Investing in the US, the definition of fiduciary matters because it is THE critical point of contention around the misunderstanding of the different investment styles. That term was the consistent theme on both sides as they talked past each other. I counted 'fiduciary’ 78 times in the video transcript, which means it was mentioned approximately every 2 minutes throughout the hearing.

The talking points

Even though he was a bit corny, Rep. Raskin kicks us off with one key point about being a fiduciary:

…the whole point of being a fiduciary is to be vigilant, watchful, and alert to opportunities and risks, and that's what asset managers, corporate board members, and executives do with other people's money.

As the Majority witnesses began, it was clear that values and conspiracy would rule the conservative talking points. For example, Marshall said this in his opening statement:

ESG is a clear and present danger to consumers and to our democracy. An unelected cabal of global elites is using ESG to hijack our capitalist system, capture corporations, and threaten hard-earned dollars of American workers. Since President Trump's election, the global elites have formed at least ten alliances dedicated to implementing radical ESG plans.

‘Global elites’ was said a dozen times.

One true thing is the callout of pressure around those alliances. The three alliances that kept coming up during the hearing were Climate Action 100, GFANZ, and NZAM. However, these groups are focused on net-zero and sustainability efforts, not material Environmental issues. I couldn’t find the term ‘ESG’ meaningfully appearing on their websites.

Now, not all conservative points were invalid. There are a lot of burdensome disclosures and shareholder proposals out there. Sometimes, the company may see a burden where investors see an ESG risk. For example, one point that came up several times was that Trillium Asset Management sent a shareholder proposal for a racial equity audit at Travelers, the insurance company. Any audit is a burden to complete as it takes employee time and costs money. However, these racial equity audits can uncover risks that companies must address. For example, Key Bank was recently named the worst lender for Black borrowers. They disagreed with the findings but are executing such an audit to uncover more information before shareholders bring the proposal forward.

It is interesting to watch ESG get forced into black-and-white issues because it doesn’t quite fit.

I’m not going to go through the entire hearing because there was a lot, and ultimately it boiled down to two perspectives:

Liberals saw ESG for what it is in some cases in its relationship to fiduciary duty. However, they often also ascribed values to ESG, which is probably fair due to the complexities. I wasn’t convinced many in the room besides Frerichs understood ESG Investing, as he was stellar and consistent.

Conservatives believe that there is liberal influence forcing values on companies to support climate change, DEI efforts, and other agendas. As a result, these values would cost pensioners money over the long term, not be a fiduciary responsibility, and even obfuscate how their money is being used. Along this last point, Rep. McClain said it isn’t always clear that a Financial Services firm (or company) has entered into an “ESG pledge,” which I took to mean a sustainability commitment.

Crockett makes an excellent argument

This exchange with Rep. Crockett showed the most precise knowledge of a committee member. I’m going to take this opportunity to call out a quick aside. Per her Wikipedia page, Crockett, like me, is a Liberal Arts major, specifically Art. She also has a Juris Doctor in law. Logically, her approach might have aligned with the Majority witnesses’ legal debate, but she drew the relevant connections to ESG data, investing, and risk wonderfully.

As Crockett leads us into her knowledge of ESG, she mentions the US Global Accounting Office’s (GAO) recent High-Risk Report and how Chairman Comer, who called the hearing, commented on the report that now "Congress can make more informed decisions." She indirectly harkened back to Frerichs’s opening statement on how ESG is data that leads to more informed decisions, nailing this point in a way her fellow committee members did not.

Here’s just a snippet of the GAO’s report, which intersects with the Environmental and Social well:

She also brilliantly calls out the underlying investments by addressing how companies report and manage ESG issues. She illustrates this by outlining how Royal Dutch Shell has dealt with ESG issues since 2005 and how even the Fox News Corporation appears to support ESG at the intersection with a material lens, not just platitudes.

Fundamental misunderstanding

Throughout Frerichs’s points, he called out how ESG helps to provide additional perspective on seemingly healthy companies like Enron and Purdue Pharma. Both are examples of poor Governance, but Purdue Pharma’s issues also intersected around the Social as they were found guilty of fueling the opioid crisis.

Republicans would do well to lean on Governance as the guidepost for defining ESG. For example, in arguing against Frerichs’s examples here, Rep. Timmons inadvertently called out how ESG works.

You reference two things that I just totally disagree with have anything to do with ESG. Litigation risk for pharma and understaffing for whatever business you're referencing. Those are not ESG.

That is a legitimate thing to take into account as it relates to the profitability of a business. If they're going to get sued and lose hundreds of billions of dollars, that is going to affect their bottom line.

Understaffing, it could result in a worse or good product, which could subject it to major challenges.

Timmons cites exactly how ESG risk works by referring to these two Social and Governance examples. His disagreement here doesn’t change what ESG actually is, it only reinforces his perception of it.

What can be done?

With these unproductive dialogues in the US, clarity is desperately needed. The EU already has the Sustainable Finance Disclosure Regulation (SFDR) to classify how funds are labeled, but it doesn’t directly address these questions about the definition of ESG. A starting point for this uniquely US problem might be the SEC's proposed rule for funds and advisors around ESG.

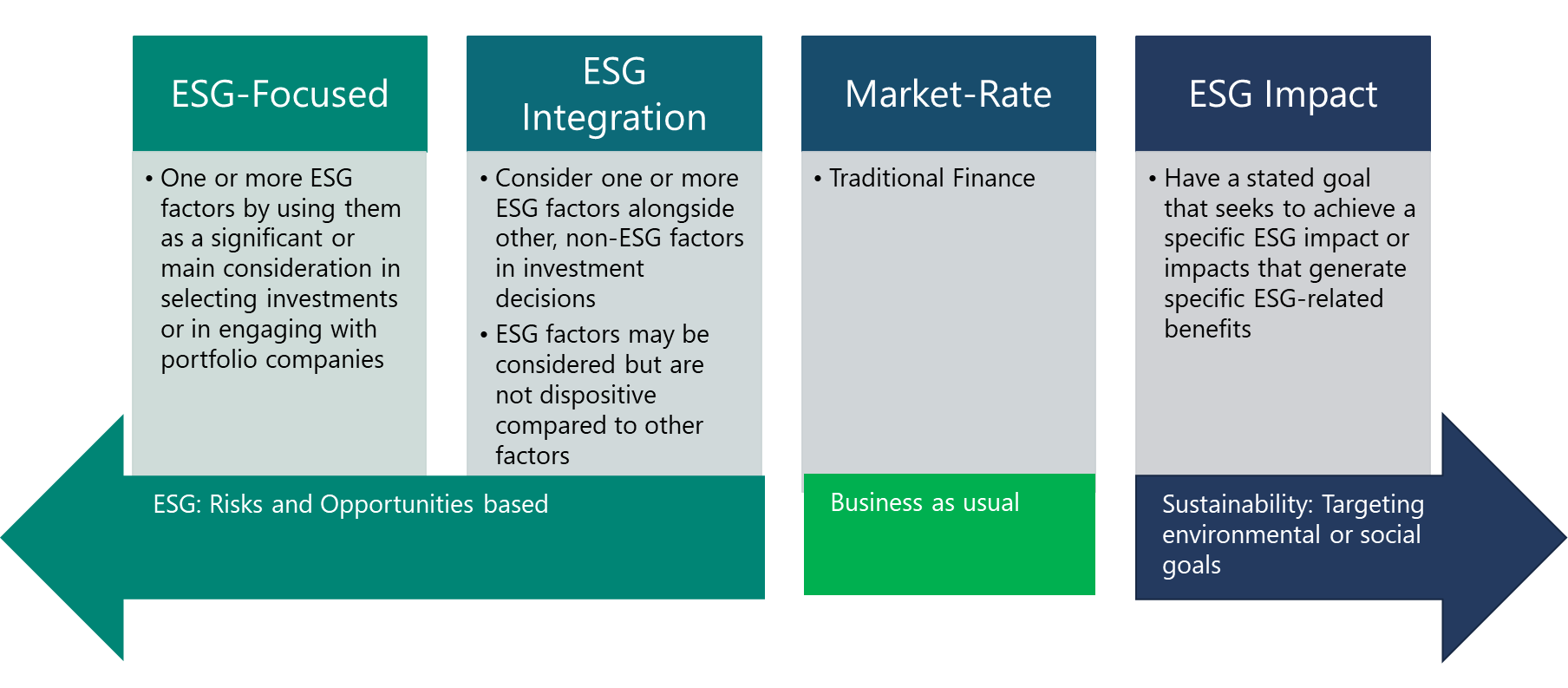

I created this handy graphic last year, which interprets the proposed rule. I can’t emphasize enough how much I believe “ESG” should be removed from “ESG Impact.” This is where the confusion lies, as having other goals besides financial returns could be interpreted as non-fiduciary.

Yet, there’s one more thing, perhaps the most giant pill to swallow. Financial Services firms must develop better transparency and communications around their investment strategies and outline what approaches it uses on which financial products. Until this clarity around ESG is understood by clients, it will be difficult to argue which funds are considering a fiduciary approach and risk versus other goals.

In fact, this issue permeates even the studies of inflows into ESG investing. While the inflows are often reported as “ESG Investing,” I have yet to see an effective differentiation between ESG, SRI, Impact, and other existing strategies. I suspect it’s because the transparency just isn’t there.

All of this confusion is leading conservative states to throw the investing baby out with the bathwater by restricting or banning entire institutions when the reality is more nuanced than that. The result is transient political talking points and long-term costs for pensioners in the hundreds of millions.

Financial Services firms must also clarify their sustainability commitments and the expectations around Scope 3, Category 15 (Financed Emissions), concerning the firm’s varied investment strategies. For example, if a firm has a net-zero commitment, it is a logical leap to think that fossil fuel divestment is the leading strategy. Outlining divestment, transition, engagement models, and/or carbon removals may help alleviate political concerns.

Steps like these allow a firm to participate in several investment strategies, including continuing to use ESG data to make more informed investment decisions and support an investor’s values. While wading into this political debate may seem unnatural, I think firms have opportunities to do so indirectly by addressing labeling and strategies around the talking points. Firms need to act like they are doing different things because they are. In ignoring these pressures, the industry is creating an ESG risk of its own making, eventually putting them in front of Congress next.

Resources

You can watch the hearing here. I recommend 1.25x speed.

If you want to read more about the ‘cognitive dissonance’ of the hearing, check out Congress’ ESG Hearing: This is Weird.

Check here to see a list of banned Financial Services firms by state.

Lastly, if you found the Governance exchange interesting, I discussed its importance on Workiva’s ESG Talk podcast on Friday. Don’t miss it!